Share this post:

Quick summary: Dubai Property Payment Plans

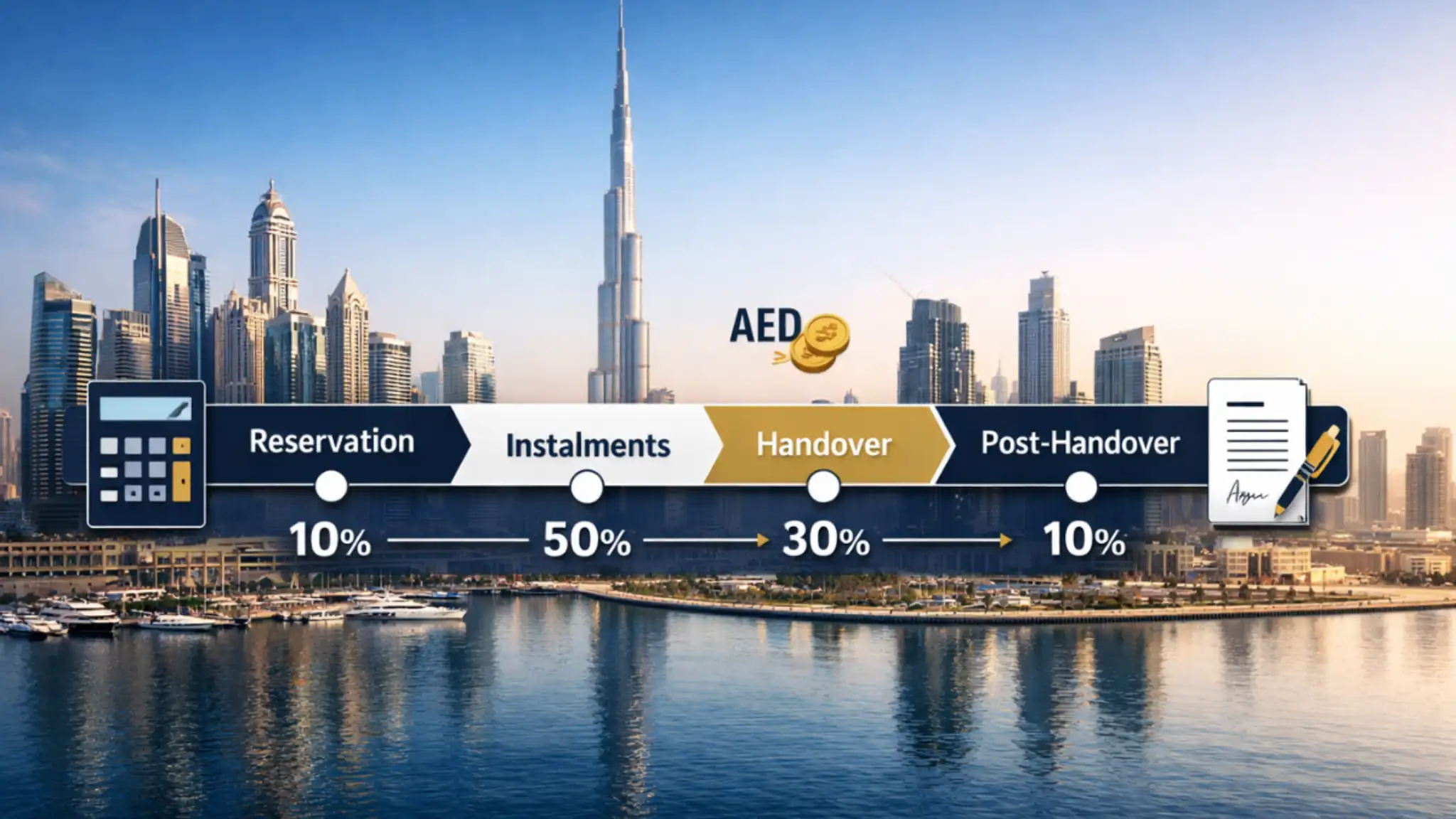

Dubai Property Payment Plans let international buyers spread the purchase price across clear milestones, rather than paying everything upfront. In practice, you will usually see a booking / reservation amount, then staged instalments during construction (or before transfer), and a final payment on handover (or on title transfer for ready property).

- Most common structure: 10–20% to secure, then staged payments, then a balance at handover.

- Off-plan vs ready: off-plan plans are milestone-based; ready homes typically need a larger amount at transfer, unless developer instalments apply.

- What to budget beyond instalments: transfer / registration, agent commission (if applicable), mortgage fees (if using finance), service charges, and DEWA / move-in setup.

- Best use-case: buyers who want flexibility, but still want the discipline of a documented schedule.

The key is to treat the payment plan as one part of the overall cost. A “low monthly” headline can look attractive, but your real decision should be based on total price, fees, handover risk, and resale / rental demand.

Not sure which payment plan is actually safe for your situation?

Share your budget, timeline and residency plans, and our Dubai Light Haven team will help you compare instalment schedules, fees and risks before you pay a reservation fee.

How Dubai Property Payment Plans work (in plain English)

If you are buying from abroad, Dubai Property Payment Plans can feel refreshingly straightforward compared with some markets. Most developer-led plans are written into the Sales Purchase Agreement (SPA) and set out exactly when you pay and how much you pay at each stage.

In simple terms, you are agreeing to pay the price in chunks. Those chunks might be triggered by construction milestones (off-plan), by calendar dates, or by the legal transfer / handover event.

Typical stages you’ll see on a Dubai payment plan

- Reservation / booking (sometimes called EOI): paid to secure the unit and start paperwork.

- Down payment: commonly paid on SPA signing or shortly after.

- Construction-linked instalments (off-plan): paid at defined milestones (for example, foundation, structure, façade, etc.).

- Handover payment: due when the developer completes the property and invites you to handover.

- Post-handover instalments (some plans): a portion paid after you receive keys, usually over a fixed period.

If you want a broader view of the overall buying process, you may also want to read our guide on the full buying journey for foreign buyers before you choose a plan.

Quick snapshot: what “real cost” usually means alongside instalments

- Plan payments: the staged instalments you owe to the developer (or seller) under the SPA.

- Transfer / registration: typically due around title transfer (ready property) or at registration steps for off-plan.

- Ongoing ownership costs: service charges, utilities setup, and furnishing (if you plan to rent or move in).

We keep this guide intentionally practical: you will see fewer hard numbers and more decision logic, because fees and promotions can change by developer, project and timing.

Types of Dubai property payment plans you’ll see

Not all instalment schedules are created equal. Below are the structures international buyers most commonly come across, with the trade-offs explained in normal language.

1) Standard off-plan milestone plan

This is the “default” for many new launches. You pay a booking amount and then make staged payments as construction progresses, with a larger portion due at handover.

- Best for: buyers who want time to build equity while the project completes.

- Watch for: whether milestones are clearly defined and whether the handover date is realistic for your timeline.

If you are comparing options, our guide to off-plan projects and real costs can help you frame the decision beyond the headline plan.

2) Post-handover payment plan

Some developers offer plans where a portion is paid after you receive the keys. This can reduce pressure at handover, and in some cases it can align with rental income if you plan to let the property.

3) Ready property instalments (developer or seller-led)

Ready properties usually require a larger portion at transfer. However, certain developer offerings (and some negotiated deals) can still include instalments. These are less common than off-plan, but they do exist.

- Best for: buyers who want immediate use (renting or moving in) and do not want construction risk.

- Watch for: how the transfer process works and which payments must be cleared before title transfer.

4) “Monthly payment” marketing plans

You will see ads for “Dubai property monthly payment” options. Sometimes these are genuine monthly instalments, but often they are simply the milestone plan broken into smaller calendar payments. That can still be helpful, but the underlying obligations remain the same.

What’s included in a Dubai payment plan (and what is not)

A common mistake is assuming the payment plan covers the full “cost to own”. In reality, it usually covers the purchase price schedule only. Everything else sits alongside it.

Usually included

- Reservation / booking payment and the staged instalments listed in the SPA.

- Any clearly stated administrative charges that the developer lists inside the SPA (where applicable).

- Project milestone definitions (for off-plan), plus handover procedure in the contract.

Usually not included (but still very real)

- Transfer / registration and related admin (timing varies by property type and transaction structure).

- Mortgage arrangement fees (if you finance) and valuation costs.

- Service charges once you own the unit (especially relevant for apartments).

- Utilities setup and any move-in deposits.

- Furnishing and snagging (often overlooked for off-plan handovers).

For a deeper breakdown of the “extras” that catch buyers out, see our companion guide on costs and hidden fees behind developer plans.

Dubai property monthly payment plans vs milestone instalments

Buyers often ask us for a Dubai property payment plan calculator view of the world — meaning a predictable monthly figure, like a car payment. In Dubai, the reality is usually more “lumpy” because the plan is linked to dates or construction stages.

Here is the practical way to think about it:

- Milestone plan: you pay at construction stages. The “monthly equivalent” is only useful for budgeting, not for the legal obligation.

- Calendar plan: you pay on fixed dates, often quarterly or monthly. This can feel easier to manage, but you must still check the total due before handover.

- Mortgage payment: if you finance, the bank repayment is genuinely monthly, but you must satisfy lending rules and valuations.

Fees and real costs to budget alongside instalments

International buyers also ask: “Is property expensive in Dubai?” The honest answer is: it depends on the community and the product type, but most surprises come from fees and ownership costs, not the instalment schedule itself.

Costs that matter most for planning

- Registration / transfer-related costs: these can be significant and are usually due around the legal transfer stage (or specific registration steps for off-plan).

- Service charges: especially for apartments, these can materially affect net yields.

- Insurance, maintenance and sinking funds: varies by building and ownership structure.

- Letting setup: furnishing, snagging and photography if your plan is to rent.

If you are buying from the UK and want a realistic budget view, our guide on costs and budget checklist for UK investors is a helpful next read.

Why some Dubai property looks “cheap” at first glance

Questions like “why is Dubai property so cheap” tend to appear when buyers compare new-build Dubai pricing with mature cities elsewhere. Often, what you are really seeing is a mix of newer supply, developer promotions, and different tax structures — but that does not remove the need for careful due diligence on fees, service charges and long-term demand.

Want us to sanity-check the plan before you reserve?

Send us the payment schedule and we’ll highlight the handover amount, likely fee timings, and any clauses that deserve a second look.

Step-by-step: how to choose a Dubai property payment plan that fits

A good plan is the one that matches your cash flow, your risk tolerance, and your timeline — not the one with the most attractive headline. Here is the process we use with international buyers.

Checklist: choosing the right plan (practical, not theoretical)

- Clarify your objective. Are you aiming for rental income, capital growth, a future move, or a visa / residency plan?

- Set a “handover comfort number”. Decide the maximum lump sum you can realistically pay at handover or transfer.

- Map instalments to your cash flow. If income is in GBP (or another currency), plan buffers for FX swings.

- Budget the extras. Add registration/transfer costs, service charges, furnishing and move-in setup so you are not forced into rushed decisions later.

- Stress-test the timeline. If the project completes later than expected, can you still carry the plan?

- Check resale flexibility. Ask what happens if you need to sell before handover, and what fees or approvals apply.

- Confirm how the SPA defines milestones. The clearer the milestones, the fewer surprises during construction.

If you are also thinking about residency planning, it is worth aligning your timeline with our Dubai visa requirements guide, because entry rules, documentation and timing can influence when you want the property to complete.

Common gotchas with Dubai property instalment plans

Most buyer regret is not caused by the concept of instalments — it is caused by not reading the schedule as a cash-flow plan. These are the issues we flag most often.

1) Confusing instalments with affordability

Instalments spread timing, but they do not automatically make the total price good value. Always compare like-for-like: same community, similar view / layout, similar building quality, and comparable service charge expectations.

2) Underestimating service charges

For apartments, service charges can materially affect net yield. A plan might look appealing, but the ongoing running costs determine whether the investment works.

3) Currency risk for international buyers

If your income is not in AED, the real “monthly cost” can move. It is sensible to keep a buffer so you are not forced to convert currency at the worst possible moment.

4) Assuming all developers treat resales the same

If you might sell before handover, ask early what the developer requires (approvals, admin fees, and whether the buyer must meet certain criteria). This matters more than people expect.

If you want a broader due diligence lens (beyond the instalments), we also recommend reading our due diligence checklist before paying a deposit.

FAQs: Dubai Property Payment Plans

How do Dubai property payment plans work?

Most plans follow a staged schedule written into the SPA. You usually pay a reservation amount to secure the unit, then instalments on set dates or construction milestones, with a larger balance due at handover (or at title transfer for ready property). Some projects also offer post-handover instalments, where a portion is paid after you receive keys.

Are “Dubai property monthly payment plans” actually monthly?

Sometimes yes, but often the developer is simply splitting milestone instalments into smaller calendar payments. It can still help budgeting, but your legal obligations are defined by the SPA schedule, so always check the total due before handover and the timing of larger lump sums.

Can I get a Dubai property payment plan calculator figure before I choose?

Yes — and you should. The practical approach is to convert the instalment schedule into a month-by-month cash-flow plan, then add expected fees and ownership costs. That way, you are budgeting for the real picture, not just the developer instalments.

What fees sit alongside the payment plan?

Typically, you should budget for registration / transfer-related costs, service charges, utilities setup, and furnishing if you plan to rent or move in. If you use a mortgage, add valuation and arrangement costs as well. A payment plan is usually not the full “cost to own”.

Is Dubai property expensive compared with other markets?

Dubai has a wide range: some areas and products compete with global prime pricing, while others are positioned for entry-level investors. What matters is the total value proposition for your strategy — including fees, service charges, rental demand, and how liquid the unit will be if you need to sell.

Why is Dubai property sometimes described as “cheap” online?

People often compare Dubai new-build supply with older, space-constrained cities elsewhere. Developer incentives and different tax structures can also affect headline pricing. However, “cheap” can be misleading if you ignore service charges, finishing quality, location fundamentals, and realistic rental demand.

Do off-plan payment plans automatically mean higher risk?

Off-plan has a different risk profile because you are buying something that is still being built. The right way to manage that is to focus on the developer track record, the contract terms, and whether the timeline matches your plans. Off-plan can be sensible, but it should be a deliberate choice, not a default.

Want a second opinion before you commit?

If you send us the payment schedule, we’ll help you spot the true handover amount, the fee timings, and the clauses that matter most for overseas buyers.

Next steps & useful guides

If you want to go deeper than instalments alone, these guides are the most relevant next reads:

- A deeper look at developer plans, real costs and hidden fees

- Off-plan projects: handover, payment stages and what to check

- A step-by-step buying process for foreign buyers

- A practical guide to buying on instalments as a foreign investor

- Dubai visa documents, costs and timelines (step-by-step)

- What a payment plan is A documented instalment schedule (usually inside the SPA) showing when and how much you pay.

- Most common structure Reservation / down payment, staged instalments during build (or before transfer), and a balance at handover / transfer.

- What buyers miss The plan often excludes transfer / registration costs, service charges, utilities setup, and furnishing.

- Best decision filter Choose the plan that fits your handover cash requirement, timeline, and risk tolerance — not the lowest “monthly” headline.

Ready to choose a payment plan with confidence?

Contact Plans Made Easy through Dubai Light Haven and we’ll help you compare instalment schedules, understand the true costs, and move forward with a clear plan.

Performance Verified ✅

This page meets PME Optimisation Standards — achieving 95+ Desktop and 85+ Mobile PageSpeed benchmarks. Verified on